Rohit has recently received his admission letter from NMIMS for pursuing an MBA degree. he was excited about studying in one of the best Management institutes in India. To cover his tuition fees and living expenses, he decided to take an education loan. While reading the terms and conditions, he got to know about the moratorium period.

Now Rohit is confused about what it means. Is it a delay in repayment, and does it affect the interest period? This type of question was coming to his mind. The moratorium period is a break from loan repayment. It starts after you take the education loan and lasts till you finish your course or a bit later. During this time, you don’t need to pay anything back.

If you are also planning to take an education loan, then you must know “What Is a Moratorium Period in Education Loans and How Does It Work?” to help you with this thing we are going to explain everything about it.

What is the Moratorium Period in Education Loans?

The moratorium period is a period when you don’t need to repay the loan. Because when you took an education loan, the bank already knows that you are studying currently, and you don’t have any income for now. So, to release the financial stress, it gives a gap where you don’t need to repay the loan, and this given time is called the moratorium period.

This period usually includes the full length of your course and a few extra months after that (like 6 to 12 months). The extra time given by bank helps you find a job and get settled before you start paying back the loan.

Quick Definition:

Moratorium Period in Education Loan: A repayment holiday during which students are not required to pay EMIs, usually covering the course duration plus an additional 6–12 months post-study period.

How Does the Moratorium Period Work?

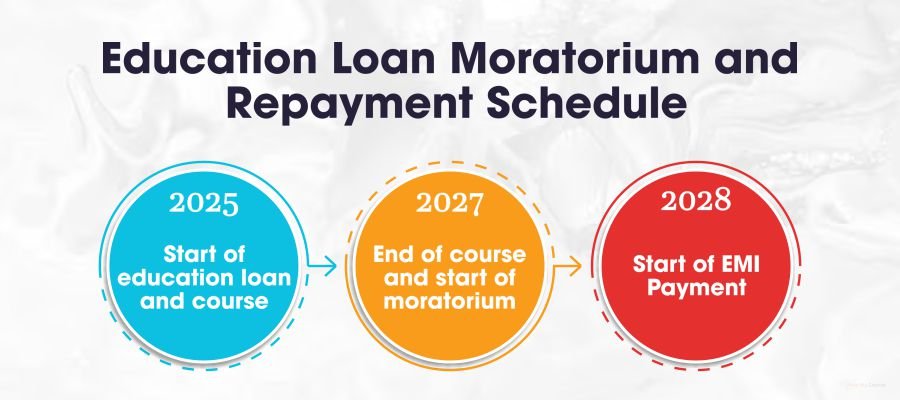

Let’s start with an example to make you understand better. You take an education loan in 2025 to study for a 2-year Online MBA course. Your course will end in 2027. Now, the bank gives you a moratorium period which includes your 2 years of study plus 6 more months after your course ends so you can settle yourself and start earning. This means you won’t need to start repaying your loan until the beginning of 2028.

During this time, most banks don’t ask for any repayment from the borrower. However, some banks may give you the option to pay simple interest during this period, if you can afford it. It’s not compulsory, but paying the interest early can reduce your overall loan burden during the repayment period.

Once the moratorium period ends, your EMIs (monthly loan payments) will start, and you will have to begin repaying the full loan as per the schedule shared by the bank.

Tenure of Moratorium Period in Banks

When it comes to education loans, different lenders have their own rules for the moratorium period and repayment. Here are how different banks and financial companies treat the moratorium period:

- Public Sector Banks:

In government banks, the moratorium period usually includes the course duration plus an extra 6 months. During this period, students don’t need to repay the loan, which gives them time to finish their course and find a job before starting repayment of the loan.

- Private Sector Banks:

Private banks have a different approach. While they offer a moratorium period, it’s not entirely payment-free like in government banks. Repayments, including part of the principal, begin after the moratorium. Private banks may also allow students to pay some interest during this period, unlike public sector banks. It will lessen the loan burden.

- NBFCs (Non-Banking Financial Companies):

For loans from NBFCs, the moratorium period typically lasts for the course duration plus an extra 12 months. However, during this period, you may be required to pay simple interest or some partial interest during the moratorium period.

Note: Both private banks and NBFCs also check your financial background before approving such payments, so it’s important to be aware of their specific requirements.

Is interest Charged During the Moratorium Period

Yes, Interest is usually charged during the moratorium period. The banks start charging interest from the date of loan disbursement. It means you don’t need to make any repayment during the moratorium period, while the borrower will have to pay both the principal amount and the interest during the moratorium period.

Also, some banks allow you to pay only the interest amount during the moratorium period. It can help you reduce the amount you need to pay later. Make sure you have read all the bank details and their procedure to handle the moratorium period.

Education Loan Moratorium Period Interest Calculator

To calculate your education loan EMI, you need to input the loan amount (Principal amount), Interest rate and tenure of the loan (number of months) into the loan calculator. The calculator will use below mentioned formula to calculate the EMI:

𝐸𝑀𝐼=[P × R × (1+R)^N] / [(1+R)^N – 1]

where:

- P is the Principal,

- R is the Rate of Interest, and

- n is the Tenure (duration in number of months).

You can also check the interest rate and the per-month EMI before taking a loan. You just need to experiment with different banks and their interest rates. By doing this, you can find a repayment amount that suits your budget.

Whereas interest rates of different banks are almost the same, a small difference in interest rate can save a big amount in the long term.

Use our free Education Loan EMI Calculator at MapMyCourse to compare repayment plans from different banks.

Difference Between Moratorium and Grace Period

Feature | Moratorium Period | Grace Period |

Duration | Lasts for the course duration + 6 months (sometimes more). | Lasts for a few months after the moratorium period. |

Purpose | Gives time to complete studies before loan repayment begins. | Provides extra time to prepare financially after studies. |

Repayment | No repayment required, but interest still adds. | Repayment may begin, or only interest may be due. |

Interest | Interest is added to the loan, but not due immediately. | Interest continues, and some banks may require partial payments. |

Start Time | Starts right after the loan is disbursed and lasts through your studies. | Starts after the moratorium period ends. |

Benefits of the Moratorium Period

- Financial Relief During Studies:

The Moratorium period allows you to focus on your studies instead of worrying about repayment of the loan, as you don’t need to start repaying the loan or interest during this time.

- Time to Find a Job:

After finishing the course, you get some time to find a job. This moratorium period gives you extra time without the pressure of making any payments for your loan. During this extra period, you need to find a job to pay back the loan to the bank.

- More Time to Plan Your Finances:

This moratorium period gives you time to manage and plan your finances before starting to pay the loan. At this time, you can plan how to handle loan repayments after starting work.

- Flexibility:

The moratorium offers flexibility, especially if you are not sure about when you will begin earning or if you are planning to further your education after your degree. It provides some breathing room before you begin repayments.

What Happens After the Moratorium Period Ends?

Once your moratorium period ends, it is time to start the repayment of your education loan. It simply means your EMI will begin, which includes the loan amount and the interest amount.

The bank will usually give you a fixed schedule for repayment, for example if your tenure for the education loan is 10 years so you need to pay the monthly EMIs for the next 10 years after the completion of the moratorium period.

In case you haven’t paid the interest during the moratorium period, then that interest might get added to your total loan amount, which leads to slightly higher EMIs. To avoid this, many students choose to pay the interest during the moratorium period.

Also, if you miss EMIs after the moratorium so it can affect your credit score, so it is important to pay the EMIs without any delay. If you are facing any issues, you can directly talk to the bank, they might help you with some flexible options.

Eligibility for Education Loan with Moratorium

- The applicant should be an Indian citizen and at least 16 years old.

- Applicant’s family must have a stable income source to support the loan.

- In most cases, a co-applicant is needed. This can be a parent or guardian who takes joint responsibility for the loan.

- The co-applicant should have a stable and regular source of income.

- The applicant must have secured admission to a recognised college or university, either in India or abroad. A copy of your admission letter is usually required.

- Having a good academic record can increase your chances of getting the loan approved quickly.

Documents Required

- A completed loan application form, filled correctly

- Proof of admission to the educational institution

- Mark sheets of the last qualifying examination

- Schedule of expenses for the course

- Passport size photographs

- Identity proof (such as Aadhar card, passport, driving license, etc.)

- Address proof (such as Aadhar card, utility bills, etc.)

- Income proof of parents or guardians

- PAN card of the student and parents or guardians

- Bank statements of the applicant and co-applicant for the last six months

- Collateral documents (if applicable)

- Any other documents as required by the lending institution

Related blogs

Final Thoughts

I hope you now know what is a moratorium period in education loans and how does it work. It is your course duration plus a period of 6 to 12 months, during this period you can focus on your studies and after completing your studies you can find a job make yourself stable before starting the repayment of the loan.

Ready to take an education loan? Use our Education Loan EMI Calculator at MapMyCourse to find your best-fit repayment plan

Frequently Asked Questions

Q.1 What is a moratorium period in an education loan?

Ans. It is a break you get from repaying the loan. Usually, it lasts until you finish your course, plus a few extra months.

Q.2 Do I have to pay interest during the moratorium period?

Ans. Yes, interest keeps adding up, but some banks may ask for partial payments or let it add until you start paying EMIs.

Q.3 How long is the moratorium period?

Ans. It depends on your bank. Most public banks offer a moratorium till course completion plus 6–12 months.

Q.4 Can I pay during the moratorium period?

Ans. Yes, you can. Paying interest early can reduce your total loan amount later. It’s not compulsory in public banks, but it can help.

Q.5 Is the moratorium period and grace period the same?

Ans. Not exactly. The moratorium period is longer and usually linked to education loans. The grace period is a short gap after graduation before EMIs begin.